{kind=link}

Picture supply: Getty Photographs

Transfer apart Rolls-Royce and Fresnillo — this small-cap biotech share is skyrocketing previous a number of the UK’s main development shares. Up 100% this yr, OXB (LSE: OXB) is taking no prisoners because it fights to recuperate its losses from 2022.

Between November 2021 and October 2022, the share worth crashed 78%, falling from a excessive of £16.78 to virtually £3 per share. The value continued to fall by means of 2023 however has now recovered to £4.18 — the very best it’s been in over a yr.

So what’s subsequent for the inventory?

Chopping-edge biotechnology

Beforehand generally known as Oxford Biomedica, OXB is a comparatively small £442m inventory listed on the FTSE All-Share index. The Oxford-based biopharmaceutical firm focuses on cell and gene remedy, specialising in viral vector manufacturing. It has over 25 years of expertise working with a number of the main pharmaceutical and biotech corporations globally.

Just lately it shifted to a pure-play contract growth and manufacturing organisation (CDMO), aiming to place itself as a pacesetter in viral vector providers, serving to different corporations develop and commercialise gene therapies.

Over the previous yr, its portfolio grew to incorporate 37 shoppers and 48 programmes, specializing in viral vector varieties like lentivirus and adeno-associated virus (AAV). The worth of those contracts is roughly £94m as of 31 August.

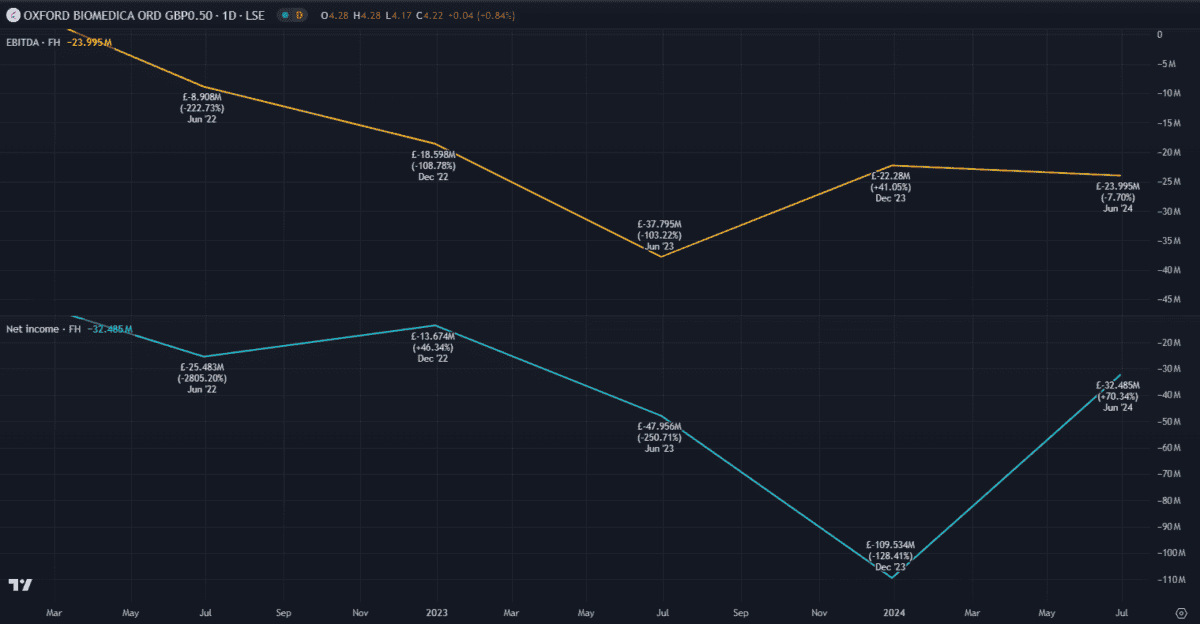

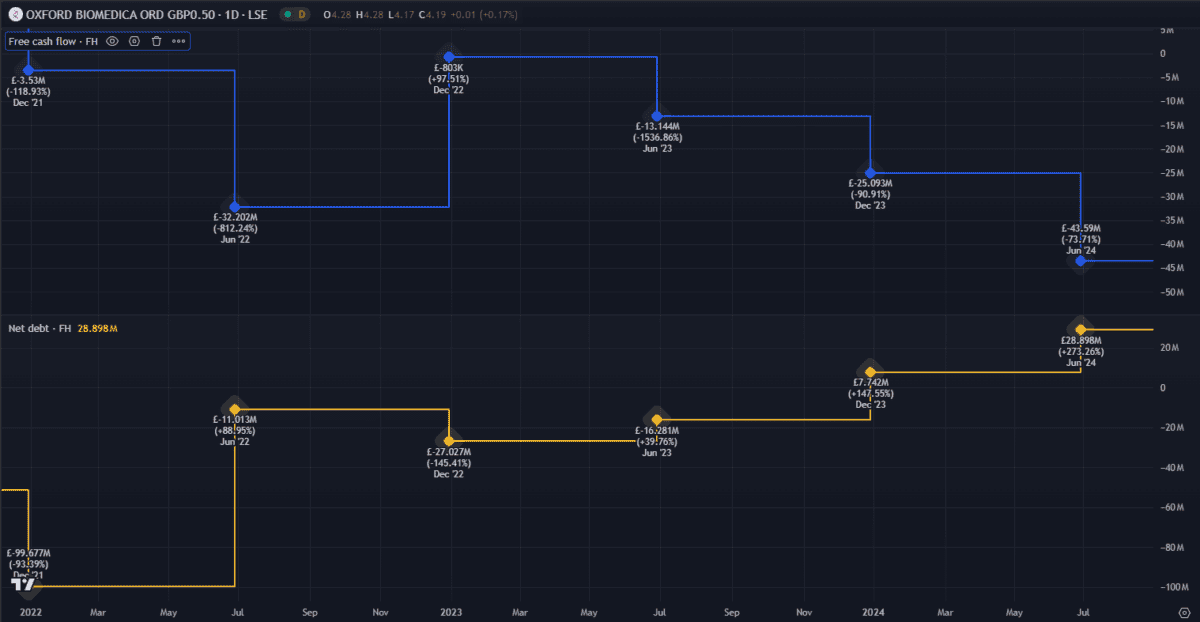

Shaky financials

Final yr was not form to OXB, with the share worth falling 50%. Within the first half of 2023, it reported a 33% drop in revenues in comparison with the identical interval in 2022. The decline was primarily because of the non-recurrence of AstraZeneca Covid vaccine manufacturing. It additionally posted an working EBITDA lack of £33.7m, larger than the £5.8m loss within the earlier yr. This was attributed to inflation mixed with larger bills associated to its new Oxford Biomedica Options division.

Issues appear to be enhancing in 2024, though first-half earnings have been nonetheless considerably disappointing. Each income and earnings per share (EPS) missed analyst expectations, by 4.7% and 110%, respectively. Though it posted a internet lack of £32.5m, this was a 32% enchancment on H1 2023.

The stability sheet appears okay for now, with a debt-to-equity ratio of 55.8%. Nevertheless, it’s burning by means of money and piling on debt, probably on account of elevated operational bills and rising bioprocessing prices.

Money and liquidity are key areas to look at as the corporate expects to interrupt even in EBITDA by the tip of 2024. In an announcement made in September in the course of the rebranding to OXB, new CEO Dr. Frank Mathias mentioned it goals to enhance its monetary standing by specializing in its position as a CDMO.

It’s unclear how effectively the change to a CDMO will repay, however the worth is already reacting positively. Nevertheless, the loss of a big shopper like Novartis may simply flip issues round. It already faces powerful competitors within the CDMO market — any drop in efficiency may lead to misplaced contracts.

If issues go effectively, the transition ought to present extra secure, long-term income versus the risky revenues from inside R&D. I anticipate it is going to proceed to do effectively so if I weren’t already a shareholder, I’d fortunately purchase the inventory at this time.