{kind=link}

Picture supply: Getty Photos

Kainos Group (LSE: KNOS) is a FTSE 250 info know-how firm specialising in digital transformation providers and Workday options.

Based in 1986 in Northern Eire, it’s grown to function in 22 nations worldwide, using over 2,900 individuals. It operates by means of three main divisions: {Digital} Providers, Workday Providers, and Workday Merchandise.

Amongst them, they cowl the digitalisation of varied purchasers within the public, industrial and healthcare sectors. Providers embrace digital advisory, cloud methods, synthetic intelligence (AI), consumer expertise design and managed providers.

However the important thing promoting level is the corporate’s partnership with Workday, a US software program system for Human Capital Administration (HCM) and Monetary Administration. Kainos builds on Workday’s choices by growing proprietary software program that enhances its performance and enhances the consumer expertise.

Years of issues

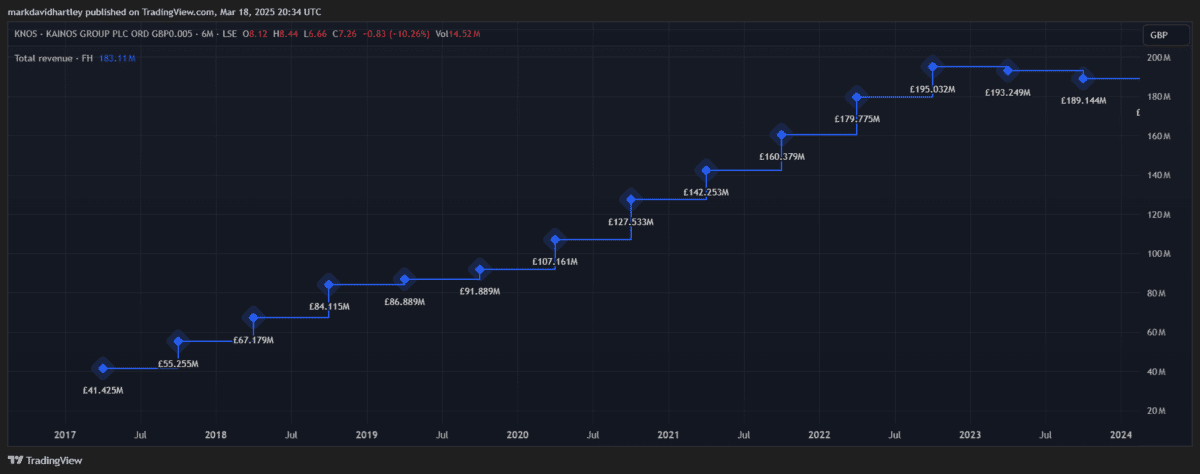

Regardless of constant income development over the previous 5 years, a slew of points have dragged down the corporate’s inventory value. It’s at present hovering round £7.27, a 65% drop from its all-time excessive of £20.52 set in November 2021.

This means it’s undervalued, with a price-to-earnings ratio of 17.4 — under the trade common of 20.7.

A number of elements have contributed to the decline, together with a weak financial system, a sudden management change and, most lately, the specter of US commerce tariffs.

The problems have led to subdued income steering for the yr ending March, additional impacting sentiment. The sudden and surprising reappointment of ex-CEO Brendan Mooney brings a wealth of expertise again in however has nonetheless irked traders. These points might proceed to restrict value development within the brief time period.

It additionally faces a barrage of opponents vying for a share of the rising digitisation market. This has led to extra aggressive pricing amongst companions, placing stress on its revenue margins and market share.

Why I count on a restoration

Kainos has established itself as a frontrunner in UK-based digital transformation and proprietary Workday providers. Regardless of rising competitors, it nonetheless instructions a big part of the market throughout numerous sectors and has a stable pipeline of upcoming initiatives that promise long-term demand for its providers.

It has overcome latest monetary struggles and maintains a powerful stability sheet with important money reserves. This monetary stability positions it properly to make the most of growth alternatives. It additionally helps its dedication to shareholder returns, with a 4% dividend yield and 68.5% payout ratio.

Its Workday Merchandise division has loved significantly spectacular development, accounting for 19% of whole income. The strategic transfer is already proving worthwhile and will scale back reliance on service-based revenue.

A renewed development technique

With Mooney again on the helm, I feel his expertise and data might reignite the enterprise and reassure stakeholders.

His steering will seemingly refocus the enterprise on rising applied sciences comparable to AI. That is important to fulfill evolving consumer wants and capitalise on new market alternatives.

With a stable enterprise and substantial money reserves, Kainos has the flexibleness to spend money on development initiatives, pursue strategic acquisitions, or just fulfill shareholders.

It has all the trimmings of a enterprise able to adapt (and thrive) in in the present day’s quickly evolving financial panorama. That’s why I’m stocking up on the shares whereas the worth is sweet!