{kind=link}

Picture supply: Getty Photographs

The UK market is filled with high-yield dividend shares that make nice choices for passive revenue. Many pay above the three.5% common yield. However progress can be vital when contemplating shares for an revenue portfolio.

One in all my favorite FTSE 250 shares is Greggs (LSE: GRG). The favored high-street bakery chain has delivered spectacular efficiency since 2014. Up 434% previously 10 years, it’s overwhelmed the broader UK market.

However previous efficiency isn’t indicative of future outcomes. So how a lot would a £10k funding immediately internet me sooner or later?

Let’s take a look.

A stable basis

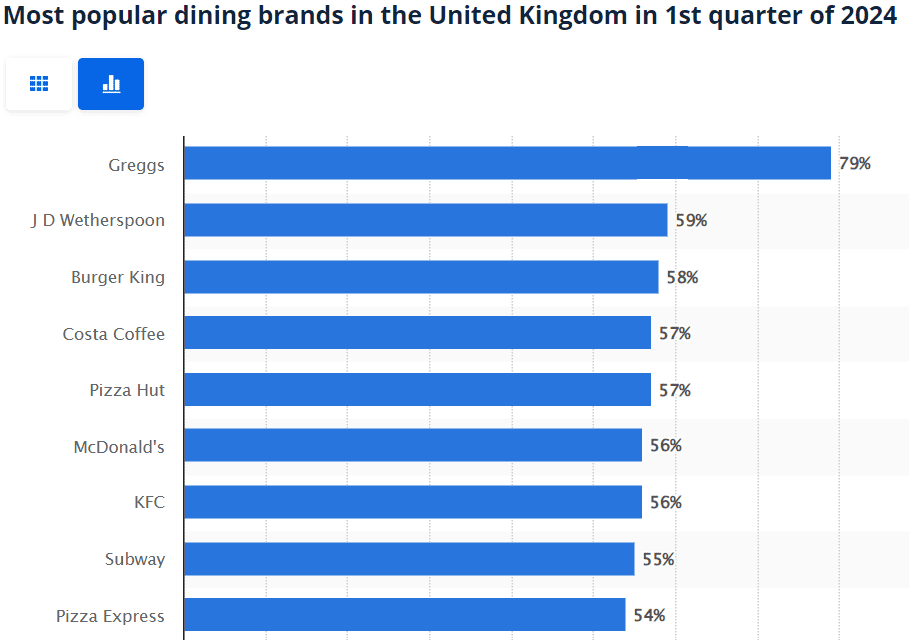

There’s little doubt Greggs is a well-loved and established British model. It’s the go-to pie and sandwich store of many hungry staff when lunchtime hits. In line with Statista, it was the most well-liked eating model within the UK in Q1 2024, beating US rivals like Burger King and McDonald’s.

What’s extra, it’s probably the most prolific. Since 2006, the variety of Greggs retailers within the UK has virtually doubled. It now has practically 2,500 outlets on excessive streets and in stations and airports throughout the nation.

With a £3.25bn market cap and £1.8bn of income final yr, it’s truthful to say the corporate has a good basis for future progress. Nevertheless, its half-year 2024 outcomes revealed a slowdown. At £55.1m, internet revenue decreased 8.6% from H1 2023 and earnings per share (EPS) decreased from 59p to 54p.

Valuation and forecasts

Taking a look at numerous metrics, the share worth is perhaps overvalued. It’s 43% above truthful worth primarily based on future money circulate estimates and the price-to-book (P/B) ratio exhibits the shares are 6.5 occasions the corporate’s guide worth. That’s not unusual amongst standard shares however might restrict progress within the quick time period. It might must submit more and more higher outcomes to usher in extra consumers at this stage.

Analysts count on income to extend by 22% over the following two years, with earnings rising by round 13%. The common 12-month worth goal is simply over £33, a 4.3% enhance from immediately’s worth.

Dividends

Dividend-wise, Greggs had monitor report previous to Covid. Funds elevated between 2000 and 2018, with solely a quick pause in 2013. They have been lowered in 2019 and reduce for one yr in 2020. Nevertheless, they returned with a vengeance in 2021, virtually doubling the 2018 payout.

Nonetheless, at 2%, the yield is low and received’t ship a lot added worth. It could pay solely £20 a yr on a £10,000 funding. Nevertheless, assuming a median 5% annual worth progress and reinvested dividends, the pot might develop over time.

With these figures, it might double to £20,000 after 10 years and pay dividends of £370 a month. It’s not a lot, however greater than a typical financial savings account would obtain.

Remaining ideas

I believe Greggs is a stable and dependable worth inventory however not an enormous passive revenue earner. My concern is that it could have tapped out its market within the UK. I believe it has potential for growth in Europe however could battle to discover a foothold within the US.

I like my Greggs shares and I’m an everyday buyer so I plan to carry them. However I’m not shopping for extra. I’m involved about the way it will develop going ahead.

I belief it has a plan.