{kind=link}

Picture supply: Getty Photos

With regards to the most effective UK inventory to purchase now, AG Barr (LSE:BAG) most likely isn’t the primary identify that involves thoughts. However I believe could be a greater candidate than it appears.

The inventory trades at an unusually low price-to-earnings (P/E) ratio and appears set for some vital progress in earnings. That’s a mixture traders ought to concentrate to.

Valuation

Let’s begin with valuation. Shares in AG Barr at the moment commerce at a P/E ratio of round 18, however that is unusually low – the inventory has sometimes traded at round 20 occasions earnings over the past decade.

AG Barr P/E ratio 2014-24

Created at TradingView

This implies the share value may improve by round 11% if the inventory can simply get again to its common over the past 10 years. However issues aren’t fairly so easy.

With out earnings progress, the inventory’s unlikely to commerce at 20 occasions earnings. I wouldn’t pay that for a stagnant enterprise and I wouldn’t count on anybody else to.

Luckily, it appears to be like like AG Barr’s earnings are going to extend over the subsequent couple of years. And this makes the P/E ratio returning to its current common more likely.

Earnings progress

AG Barr’s greatest product is Irn Bru, which accounts for round 33% of whole gross sales. It’s a curious product – nearly unattainable to disrupt in Scotland, however equally arduous to export wherever else.

That doesn’t normally make for sturdy progress prospects. Nevertheless it’s not elevated gross sales volumes which are more likely to increase the corporate’s earnings going ahead – it’s wider margins.

AG Barr Working Margin 2014-24

Created at TradingView

Again in 2022, AG Barr acquired BOOST Drinks Holdings to, um, increase its revenues. Within the brief time period, this has had a unfavorable impact on profitability, however the results appear to be carrying off.

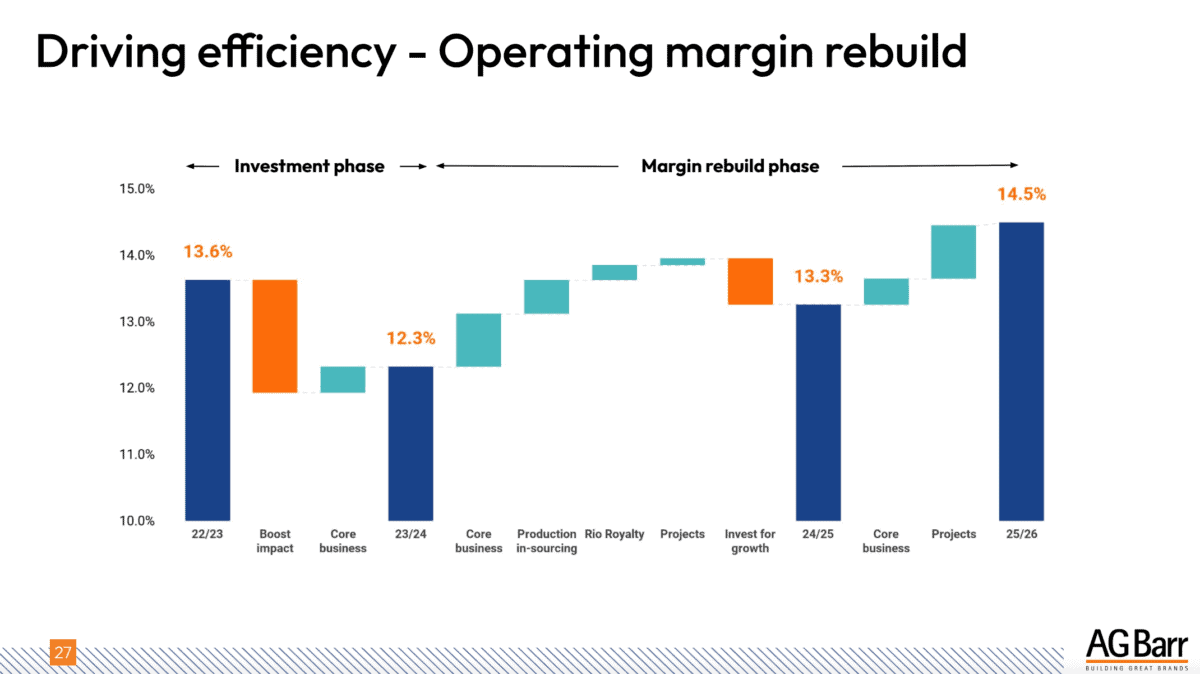

Supply: AG Barr 2023/24 outcomes presentation

The agency is anticipating working margins to increase from 12.3% in 2023/24 to 14.5% by the top of 2026. That doesn’t sound like loads, but it surely quantities to an 18% improve in earnings.

A 30% return?

Briefly, I believe the shares may go from a P/E ratio of 18 with 12.3% margins to a P/E ratio of 20 with 14.5% margins by 2026. Collectively, that makes a 30% improve inside a few years.

Clearly, there aren’t any ensures. For instance, if inflation picks up, the corporate’s margins won’t develop as anticipated.

One other difficulty is rates of interest. If these keep larger for longer than traders predict, it’s much less doubtless the P/E ratio will increase in the best way I’m anticipating.

These may trigger returns to return in decrease than traders would possibly hope. And there’s not loads AG Barr (or its shareholders) can do about both.

A inventory to purchase?

It’s price noting although, that the assumptions behind the 30% determine have some margin of security inbuilt. For instance, the dividend isn’t included nothing in the best way of income progress is factored in.

Moreover, even when issues go barely worse than anticipated, even a 20% return over the subsequent couple of years is hardly a nasty outcome. Because of this, I’m seeking to purchase for my portfolio.